Loan Against Property: How to Calculate Loan Against Property & Understand Interest Rates

Using your residential, commercial, or industrial property as security against property loan is among the most reliable and flexible means of getting a substantial amount of money. A LAP provides large amount of loans, good interest rates and long-term repayment period whether you require funds to grow your business, to further your education, to pay off medical bills or to pay off your debts. This being a secured loan, the process of being approved may be easier-provided that you satisfy the requirements of your lender in terms of eligibility and valuations.

When planning to apply such a loan, it is important to know how lenders determine the loan against property, the main factors, which influence the amount of loan to take, and how interest rates loan against property are calculated. This guide will take you through all these aspects in order to make a financial decision that is well informed.

What is a Loan against Property?

Loan against property is a secured loan where you set your own property as the security to the loan. The lender will evaluate the market value of your property and offer you a loan at a percentage of the value most likely up to 70% to residential properties and slightly low to commercial ones. You still retain ownership of the property, and you can do anything you want with it but your title documents are in the possession of the lender until you can pay the entire loan value.

Some of the key features include:

High loan amount depending upon property valuation

Lower interest rates compared to personal loans

Flexible repayment tenure that may extend up to 15–20 years

Use of funds for any legitimate purpose from business to personal needs.

Because the property serves as security, lenders assume lower risk and can therefore provide more favorable terms.

How Lenders Calculate Loan Against Property

Understanding how lenders calculate loan against property helps you estimate your eligibility and plan your finances better. The loan amount is not solely based on your property’s value; several factors influence the final sanctioned amount.

1. The Market Value of the Property

This is the biggest factor. Lenders evaluate:

Location, meaning prime areas get higher valuations

Property type (residential generally valued higher than commercial)

Age and condition of the property

Market demand and resale potential

Most lenders give between 50% to 70% of the market value. For instance, if the market value of your property is ₹1 crore, then the loan amount might range from ₹50 lakh to ₹70 lakh.

2. Loan-to-Value (LTV) Ratio

The LTV ratio defines how much of the value of the property the lender is willing to finance. LTV varies depending on:

Internal lender policy

Property classification

Borrower’s creditworthiness

Commercial buildings, old properties, or properties in semi-urban areas get lower LTV.

3. Income and Repayment Capacity

Even though this is a secured loan, lenders ensure that you can comfortably repay the EMI. They assess:

Your monthly income

Existing debt

Employment security

Business performance (for self-employed applicants)

Typically, your EMI should not exceed 40%–50% of your monthly income.

4. Credit Score

A good credit score is considered above 750 and ensures a higher loan amount. A lower credit score makes your loan vulnerable to less amount or higher interest charges.

5. Ownership of Property and Documentation

Clear ownership, updated paperwork, and no legal disputes on your property improve your loan eligibility. Any mismatch may decrease the sanctioned amount.

How to Calculate Loan Against Property Yourself

Many lenders offer online LAP calculators that help in assessing the loan amount and EMI. You can calculate a loan against property manually using:

Step 1: Estimate Property Value

Get a realistic idea from:

Local real estate trends

Professional valuation

Comparable properties in your area

Step 2: Apply LTV Ratio

Use an approximate LTV of 60–70%.

Example:

Property value: ₹80,00,000

LTV: 65%

Estimated amount of LAP = ₹52,00,000

Grammar practice

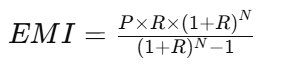

Where:

P = Loan amount

R = Monthly interest rate

N = Tenure in months

EMI calculators automate this to help you compare tenures and interest rate scenarios with ease.

Interest Rates Loan Against Property: What Affects Them?

Understanding the interest rate on loan against property will help you select the right lender and reduce your borrowing costs. LAP interest rates vary based on many factors.

1. Property type

Usually, residential properties attract lower interest rates compared to commercial or industrial properties due to higher market stability.

2. Borrower Category

Salaried people usually get lower rates because of their stable incomes.

If income is irregular, self-employed professionals or business owners may be subject to slightly higher rates.

3. Credit Score

A good credit score reduces your interest rate by as much as 1–2%. The lower the score, the higher the risk loading and, therefore, the rate.

4. Loan Amount and Tenure

Larger loans at times fetch better price.

Longer tenures increase the rate only slightly because of extended risk exposure.

5. Type of Interest: Fixed or Floating

Fixed Rate: Stable Monthly EMI, Slightly Higher.

Floating rate: Lower initial rate but changes with market conditions.

6. Lender’s Internal Policies and Market Conditions

Economy-wide interest rate movements, RBI policies, and lender strategies also impact the pricing of LAP.

Benefits of Taking a Loan Against Property

1. High Loan Amount

Because the loan is secured, you can borrow large sums—ideal for business expansion or major expenditures.

2. Lower Interest Rates Compared to Personal Loans

The interest rates for LAP are usually much lower, hence it is cost-effective for a long-term borrowing perspective.

3. Long Repayment Period

The tenures range up to 15–20 years, thus minimizing EMI burden and increasing affordability.

4. Continue Using Your Property

You do not lose ownership or usage rights. Only the documents remain with the lender.

5. Flexible Use of Funds

The loan amount can be utilized for any personal, professional, or business-related reason.

Tips to Get the Best Loan Against Property Deal

Shop around with different lenders to find the best interest rates and lowest fees.

Improve your credit score before applying

Choose the right tenure to balance the EMI with the total interest payable. Negotiate processing fees and valuation charges Maintain strong income documentation

Conculasion

A loan against property is a strong financial solution when one needs large amounts of money with feasible payback options.Knowing the way lenders price loan against property and what influences the interest rates of a loan against property, you are now in a position to make sound decisions. It is flexible, cheap and stable in the long term whether through business expansion plans, high-value expenses, or debt consolidation, LAP provides the best.

FAQ

Can I use a loan against property for any business purpose.

Yes, you can use the funds from a loan against property (LAP) for various business purposes, including expansion, purchasing equipment, or covering operational expenses, as there are no restrictions on its usage.

What property can be used as collateral for LAP.

Both residential and commercial properties can serve as collateral for a loan against property. This includes homes, apartments, offices, and retail spaces, providing flexibility in securing financing.

How much loan can I get against my property.

The loan amount typically ranges from 50% to 75% of the property’s current market value. The exact percentage may vary based on the lender’s policies and your financial profile.

Can LAP be availed by self-employed individuals.

Yes, self-employed individuals, including professionals and business owners, can apply for a loan for business against property, provided they meet the lender’s eligibility criteria, such as credit score and income stability.

Good knowledge about LAP